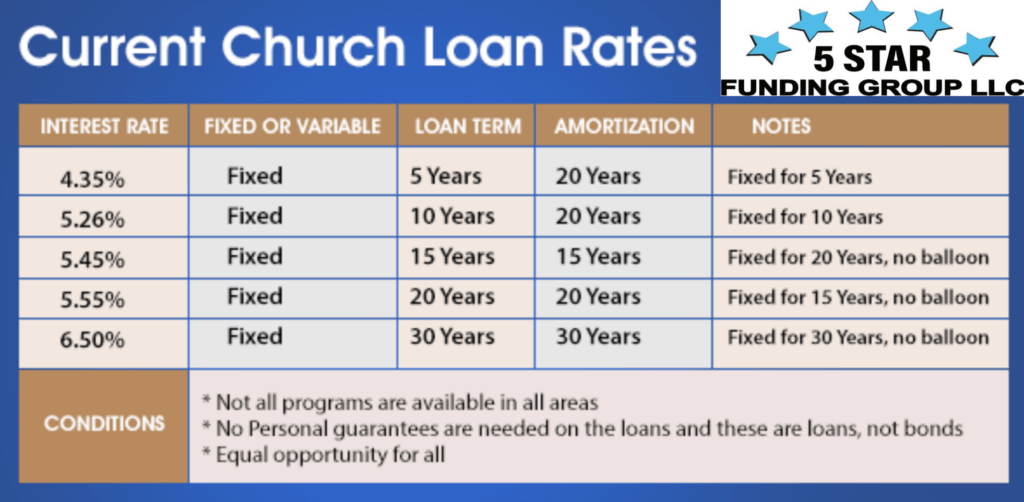

Church Financing and SBA Loans

Church Financing and SBA Loans

There are other differences between the church financing products we offer and traditional loans. Some traditional commercial properties, like owner occupied, or mostly owner occupied commercial real estate qualify for SBA Loans. SBA loans are loans are guaranteed by the government so if the mortgage is not paid and the lender has to foreclose on the property owner, the government will make the lender whole for any losses they sustain. Non-profit organizations including churches, do not qualify for SBA loans under normal circumstances. The exception to this rule is during times of emergency, where the SBA issues Disaster Relief Loans (think Hurricane Katrina).

Foreclosure

When a traditional for profit borrower falls behind on its payments to a lender, it will often find out quickly that most lenders are unforgiving and will take legal action to protect their interests including foreclosing on the property very quickly. This is where churches benefit from the type of organization they are. In many instances, a traditional lender that would not think twice about taking a property from a traditional business will work with a church when they get into trouble. Often a lender will give the church interest only payments for a period of time, allow them to tack on past due payments to the end of a loan, wave penalties, among other things. However, when the lender decides that they have done all they can and the church is still unable to make the payments then foreclosure is probably eminent.

Private Money Loan

If a church finds itself in a position where its payments are late and they are unable to refinance with a traditional loan or borrow money from members then one of the last options is a Private Money loan. There are very few companies in the country that offer Private Money Loans to churches, and we happen to be one of them. We offer traditional loans with great interest rates and loan terms,and when a church is in trouble, we have a solution. The Private Money loans we offer are lenient and creative and can often be closed extremely quickly.

Seller Held Second Trusts

Using Seller Held Second Trusts in conjunction with traditional church financing. A Seller Held Second Trust is a loan from the seller of a property to the buyer of the property for a portion of the total amount the buyer is borrowing. In most cases, the church loans we offer have a maximum Loan to Value of 80%, what this means is that if you are buying a property for $1,000,000 the lender will agree to loan to the church $800,000 and you need to come up with $200,000. What if you don’t have $200,000 and you cannot raise the shortfall quickly? Sometimes a seller will agree to loan you some of the shortfall so it may be possible to have the church put down 10% of the purchase price and the seller hold 10% of the purchase price and the lender carry the rest.

Subordinate Position

The loan from the seller of the building to the church is in a subordinate position to the loan from the lender. Being in a subordinate position means that if something goes wrong and the lender has to foreclose and take the building, the seller loses all of their money before the lender loses any of their money. If there is enough money to pay off both the lender and the seller, then the seller will be paid off also. But, if there is a loss, all of that loss is bore by the property seller before the lender incurs any loss. There are lots of nuances to using a seller held note and they do not always work and for purposes of describing how the process works, I have greatly simplified things here.

Church Construction Loans

5 Star Funding Group offers church construction loans that are looking to build almost any type of building:

- Sanctuary,

- Family Life Center

- Gymnasium… just to name a few

Types of Church Construction Loans We Offer

We offer 4 types of construction loans for churches

- Financing for Churches that already own property and want to build a new building or an addition.

- For Churches that want to buy land and build a new building.

- Financing for Churches that want to buy a property that already has a building on it and build an addition to that property.

- For Churches in the middle of a construction project and have run out of money and the project has stalled.

Benefits of Church Construction Loans

Most of our church construction loan programs have the following benefits:

- Finance up to 100% of the project cost as long as the total project cost does not exceed 80% of the as completed value of the property. This is good for churches that do not have or do not want to use their cash but already own land that they want to build on.

- No Personal Guarantees are usually needed on our church loans.

- No audited financial statements are usually needed.

- Interest only payments during construction.

- Loan turns into a permanent loan on completion of the construction. So, there is only one loan closing, saving the church money.

- Low interest rate and great church loan terms.

What is the maximum amount of money a church can afford to borrow?

Underwriters take many factors into consideration when determining the maximum borrowing capacity of a church. A good rough estimate of the general range a church can borrow is to take the last 12 months of gross general tithes and offerings income and multiply that number by 3 times and by 5 times and that will generally give you the low end of what the church can borrow and the high end of what the Church can borrow. As an example if a church has gross income of $500,000 per year they can probably borrow between $1,500,000 and $2,500,000

Construction Completion of a Church in Progress:

Each year, we have the great fortune of working with thousands of churches and some of those are in difficult situations; one of the most difficult situations is a stalled construction project. Whether the church ran out of money, has cost over runs or their lender is refusing to honor the draw requests, we can likely help. Over the years we have provided financing to help finish churches that are unable to complete their construction project because of a lack of funding.

If your church is looking for a construction loan, we want to help, our advice is free whether we provide the financing for your project or not.

Private Money

5 Star Funding Group Offers Private Money Loans for Churches

Although most of the churches we work with have excellent credit and qualify for low-interest rates and great loan terms , there are times when churches fall into financial trouble. When a church falls into financial trouble it can be extremely difficult for them to work their way out, traditional lenders will not make loans to them and private money lenders do not accept church properties as collateral. We created a fund specifically designed to solve this problem by raising money through private investors that are looking to earn above market returns on well collateralized real estate loans.

Private Money Church Loans | Benefits of Borrowing from Us:

- Bankruptcies and foreclosures are accepted

- No minimum credit score

- No application fees

- Interest only options available to keep the payment low

- No large upfront fees

- Speed – Closings in as little as 2 weeks

- Short term and long term loans

- Discounted note payoffs are accepted

Our Loan Terms:

- Maximum loan to value of 60% on Private Money and 85% on good credit deals

- Amortizations are flexible and include 30 years and interest only payments

- Loans with no payments during the term are available (with proper exit strategy)

- Interest rates vary depending on risk

- Points vary depending on risk

- No personal guarantees are generally needed